{kind=link}

How to Write a Check Like a Pro – In the age of instant transfers and contactless payments, checks might seem like relics of a bygone era. While it’s true that digital payment methods are undeniably convenient and increasingly popular, checks still hold a significant place in our financial landscape. According to a study by the Federal Reserve, over 14 billion checks were still written in the United States in 2021. So, why are checks still relevant?

There are several reasons. For one, some businesses, particularly small and family-owned ones, may prefer to receive payment by check. Landlords are another group that often rely on checks for rent collection. Additionally, checks can be a secure way to send money to someone who doesn’t have a bank account or isn’t set up for electronic payments.

Despite their continued use, improperly filled-out checks can lead to delays or even rejection. Bouncing a check can not only be embarrassing, but it can also incur fees and damage your credit score. So, whether you’re a seasoned check writer or haven’t touched a checkbook in years, understanding how to fill out a check correctly is an important financial skill.

In the following sections, we’ll break down the process of writing a check step-by-step, ensuring your payments are processed smoothly and efficiently.

What You’ll Need

While the use of checks has declined in favor of digital payment methods, there are still situations where you might need to write one. Whether you’re paying a small business that doesn’t accept cards or sending a rent check to a landlord who prefers paper trails, knowing how to properly write a check is a valuable skill.

Here’s what you’ll need to gather before you begin:

- A check from your checking account: Look for a pre-printed check from your bank. These will have essential information already printed on them, saving you time and reducing the risk of errors. The most important pre-printed elements are:

- Routing number: This unique nine-digit code identifies your bank and is used to route the check for payment electronically.

- Account number: This identifies your specific checking account within the bank.

- Pen with black or blue ink: For the sake of clarity and security, it’s best to use a pen with black or blue ink. Banking systems easily scan these colors and are less prone to fading over time compared to other colors.

Pro Tip: Double-check your check supply. Many banks offer reorder checks online or through their mobile apps. If you’re running low, prioritize placing a reorder to avoid any payment delays.

How to Write a Check: Components of a Check

While the world increasingly embraces digital transactions, checks remain a reliable method for making payments. But for those unfamiliar, a check can seem like a mysterious document filled with cryptic information. Fear not! This guide will break down the essential components of a check, ensuring you can write secure and accurate payments.

1. Payee Line: Who Gets the Money?

The payee line is the cornerstone of a check. Here, you inscribe the legal name of the person or entity you intend to pay. This line dictates who the bank is authorized to transfer funds to. Ensuring an accurate payee name is crucial to prevent the check from falling into the wrong hands.

Pro Tip: Double-check the payee name for accuracy before finalizing the check. A misspelling could lead to delays or even the check being returned. Write the full name of the recipient on the “Pay to the Order of” line.

2. Date Line: Marking the Moment

The dateline serves a critical purpose. It establishes the validity period of the check. Typically, checks are valid for up to six months after the written date, though bank policies may vary. Postdated checks, where the date written is future, are generally not recommended as they can cause confusion and delays.

Important Note: Always date your check before handing it over. An undated check can be altered to a later date, potentially leading to fraudulent activity. Also, use the full date format to avoid confusion.

3. Amount Box: Numbers Speak Clearly

In the amount box, you write the check’s numerical value, using whole numbers and decimals for cents. This box provides a clear and concise representation of the intended payment amount.

Security Feature: It’s essential to write the amount clearly and without leaving any smudges or erasures. A clean amount box minimizes the risk of someone tampering with the number and begins at the far left to prevent tampering.

4. Amount Line: Writing it Out for Safekeeping

The amount line serves as a legal safeguard against alterations. Here, you write out the full amount of the check in words. This creates a secondary verification point in case the numerical amount is unclear or tampered with.

Real-World Example: If the amount includes cents, you can add “and 00/100” after the decimal point to clarify that it refers to cents. For example, if the price were $5.79, you could rewrite it as “5.79 and 00/100.” This is not necessary for whole numbers (e.g., $5), but it can be helpful for amounts with decimals.

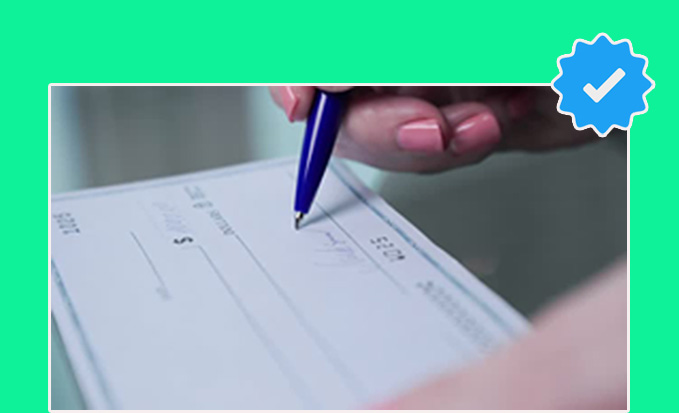

5. Signature Line: Your Seal of Approval

The signature line is where you, the check writer, provide your signature. This signature acts as your authorization for the bank to transfer funds from your account. Always sign your check with the same signature that appears on your bank signature card.

Security Reminder: Never sign a blank check. Fill out all the relevant information before adding your signature.

6. Memo Line: Keeping Track of Transactions

The memo line is an optional space for you to include a brief note about the purpose of the check. While not mandatory, this line can be a valuable record-keeping tool for both you and the recipient.

Example Use: You could use the memo line to reference an invoice number or describe the reason for the payment.

7. Routing and Account Numbers: Behind the Scenes

The routing and account numbers are a series of pre-printed numbers located at the bottom of the check. These numbers serve a crucial function: they identify the bank where your account is held and your specific account number. The routing and account numbers enable the bank to locate the correct account from which the check amount will be deducted.

Note: Never share your routing and account numbers with anyone you don’t trust implicitly. These numbers are essential for accessing your checking account funds.

Best Practices for Check Writing in the Digital Age

Just because checks are familiar doesn’t mean they’re immune to fraud or errors. To ensure your check-writing experience is smooth and secure, follow these best practices:

- Leave No Room for Alterations: Use Permanent Ink. When filling out a check, avoid pencils or erasable pens. Permanent ink makes it significantly more difficult for someone to tamper with your written information. This includes the payee’s name, amount, and even the date.

- Double-Check, Then Check Again: Verify All Information. A simple typo on a check can lead to a rejected payment or even a fraudulent alteration. Before finalizing your check, take a moment to carefully review everything you’ve written. Ensure the payee name matches the intended recipient exactly, the numerical amount corresponds to the written amount in words (including cents!), and the date is accurate.

- Keep a Paper Trail: Maintain a Check Register or Digital Record. Even in the digital age, keeping track of your checks is crucial. Traditionally, a check register was used to record check numbers, dates, payees, amounts, and memos. Today, many banks offer digital check registers within their online banking platforms. Regardless of your method, maintain a record of every check you write for easy reference and to reconcile your bank statements effectively.

- Safeguard Your Checks: Store Them Securely. Blank checks are essentially blank money, making them a prime target for theft. Keep your checks in a locked drawer or a dedicated checkbook holder, and avoid carrying more checks than you need at any given time.

- Know Your Account Balance: Avoid Overdrafts. Bouncing a check can result in hefty overdraft fees. Before writing a check, always review your account balance to ensure you have sufficient funds to cover the payment. Consider online banking or mobile banking apps to keep a real-time eye on your account activity.

Conclusion

Checks can also be a handy way to manage allowances for children, as they offer a tangible connection to money management. Remember, if you have any questions or encounter any difficulties while writing a check, don’t hesitate to contact your bank. Their customer service representatives are happy to assist you and ensure you’re using checks securely and effectively.

Keep in mind, that some banks may charge fees for using checks, so it’s always wise to consult your bank’s policy. But for those times when a check is the most suitable payment option, you’ll be glad you possess this essential financial skill!